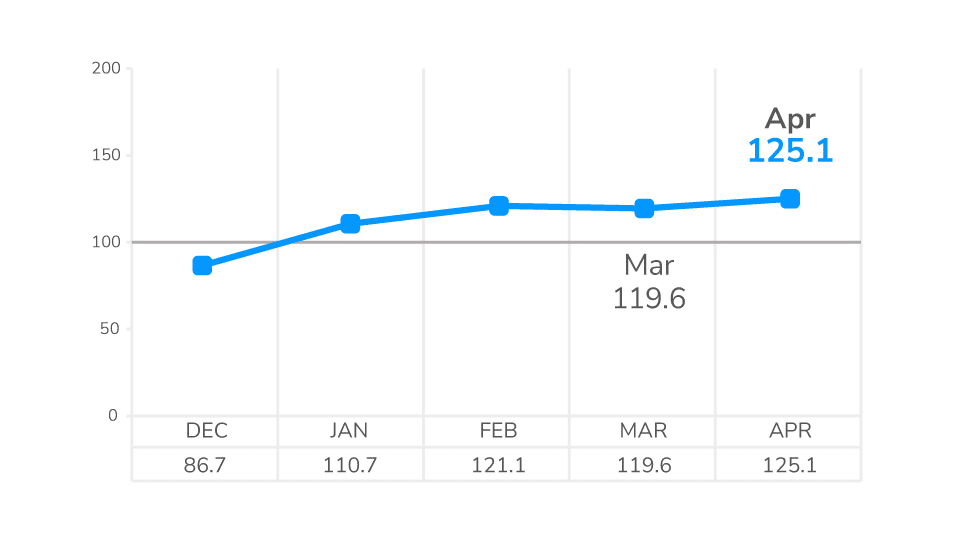

CRE Activity Holds as the Market Is Now Being Tested

Commercial real estate has moved past the question of whether activity would return. The more relevant question now is whether it can hold. April’s LightBox CRE Activity Index suggests that, for now, it can. The Index rose to 125.1, its highest level of the year and the fourth consecutive month above 100. That is a meaningful signal. After a slow 2025, the market is not just recovering. It is sustaining momentum even as conditions become more challenging.

That said, the story is no longer about acceleration. It is about durability.

From Recovery to Resilience

The first quarter followed a familiar seasonal pattern. Activity rebounded from late-2025 softness, with the Index climbing back above 100 in January and building through February and March.

April added a new dimension. Instead of retreating in response to higher Treasury yields, elevated oil prices, and geopolitical tension, the market absorbed those shocks and continued to move forward. The April Index demonstrates that the CRE market has now cleared its first real “stress test” of the year and continued to build momentum.

That shift from recovery to resilience is subtle but significant.

LightBox April CRE Activity Index at a Glance

NOTE: The LightBox CRE Activity Index is based on changes in environmental due diligence (measured by Phase I ESA volume), commercial property listings, and valuation market activity indexed to a baseline (Q1 2021 monthly average =100). The index is normalized to account for variations in the number of business days per month. The historical CRE Activity Index has been normalized to consistently include historical and current listings across LightBox platforms. The Index value reported for the most recent month may be revised in the subsequent publication as LightBox finalizes the input datasets.

The Signals Beneath the Index

The headline number is strong, but the underlying signals tell a more nuanced story.

Listings activity jumped 12% month over month, reaching the highest level since the Index began. Sellers are not stepping back. If anything, more assets are coming to market as owners adjust to current pricing stability and reposition portfolios.

Environmental due diligence continued its steady climb, with Phase I ESA activity up again for the third consecutive month. This is one of the most reliable forward indicators in the Index. It reflects deals in motion before they close, and its steady growth points to sustained deal pipelines.

Appraisal activity moved lower, down 12% from March. It remains elevated relative to longer-term norms, but the pullback introduces an important counter-signal. It suggests that lenders are becoming more selective as borrowing costs stay high, and market conditions remain fluid.

Taken together, these signals describe a market that is active, but operating with more discipline.

A Market Adjusting, Not Retreating

The broader macro backdrop helps explain this divergence.

Interest rates remain elevated, with the 10-year Treasury hovering around 4.40%. Inflation has proven sticky. Economic signals are mixed, and geopolitical developments have added another layer of uncertainty.

Under those conditions, a slowdown would not have been surprising.

Instead, the market is adjusting. Capital is still widely available, but it is being deployed more carefully. Deals are closing, but underwriting is tighter, and structures are more conservative. Investors are active across both distressed and stabilized opportunities, but with sharper focus on risk and return.

This is not a market pulling back. It is a market recalibrating.

What to Watch Next

April extends the CRE market’s strong run. The next few months will test its durability.

The split within the Index is worth watching. Strength in listings and due diligence suggests confidence is intact. Softer appraisal activity may point to tighter financing conditions.

External factors will play an outsized role. Rates, inflation, and energy markets will all influence deal timing and structure.

And yet, there is a counterbalance.

The market has largely adapted to a higher-rate environment. Refinancing demand continues to drive activity. Lending channels remain open, particularly from private capital. And transaction pipelines are still moving.

The Practical Takeaway

For brokers, investors, environmental due diligence consultants, lenders, and appraisers, the implication is straightforward: this is still an active market, but not an indiscriminate one.

Deals are happening, but they require clearer pricing, stronger underwriting, and more deliberate execution.

The Activity Index does not point to a pullback. It points to a market that is being tested and, for now, holding its ground.

Read the full April LightBox CRE Activity Index report for additional analysis and insights.

For more information about this report or the data, email insights@lightboxre.com